Auto & Motor Insurance is a big industry in the US and Europe

According to this site, State Farm is the #1 auto insurer in the US since 1942, ranked #36 on the 2019 Fortune 500 based on revenues, and has 44 million auto policies in force. From State Farm’s 2019 financial results:

“The State Farm auto insurance business represented 64 percent of the P-C companies’ combined net written premium. Earned premium was $41.5 billion (emphasis added). Incurred claims and loss adjustment expenses were $32.0 billion and all other underwriting expenses totaled $10.3 billion. The underwriting loss was $764 million.”

From Statista, the total motor premiums for the European insurance market was €144 billion in 2018.

How much of that premium is at risk from Tesla Full Self Driving (FSD)?

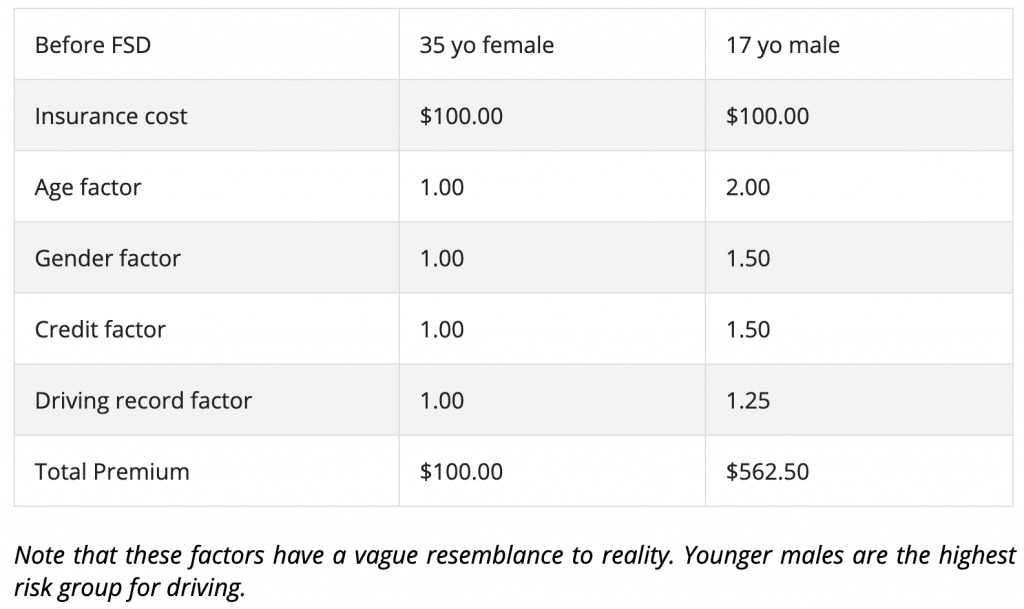

Quite a bit. Let’s go through a thought experiment. Let’s assume our first driver is a 35 year old female, with excellent credit and no history of accidents. Our second driver is a 17 year old male driver, with poor credit and one accident in the last year. Our simple model will work like this: there is a 5% chance in any given year of a $2,000 accident (we are ignoring driving distance). The pure insurance cost is $100 (5% * $2000). Various factors are applied for age, gender, credit, and accident history.

FSD changes the game

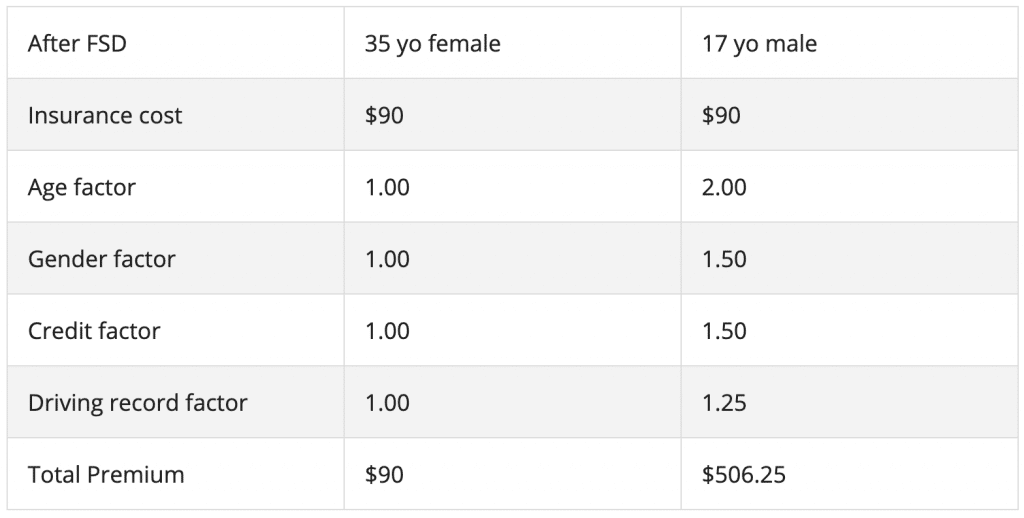

Let’s go back to our assumption. Let’s say FSD reduces the chance of an accident by 10%. We don’t know how much the drop will be, but I assume there is a drop. A 10% reduction is conservative. That means there is now a 4.5% chance of an accident, and for each accident, the average cost for claims remains $2000. The insurance cost drops to $90.

Total premiums paid drop by 10%. This is not accurate, though. Our 17 yo male, the highest risk group, will see large benefits.

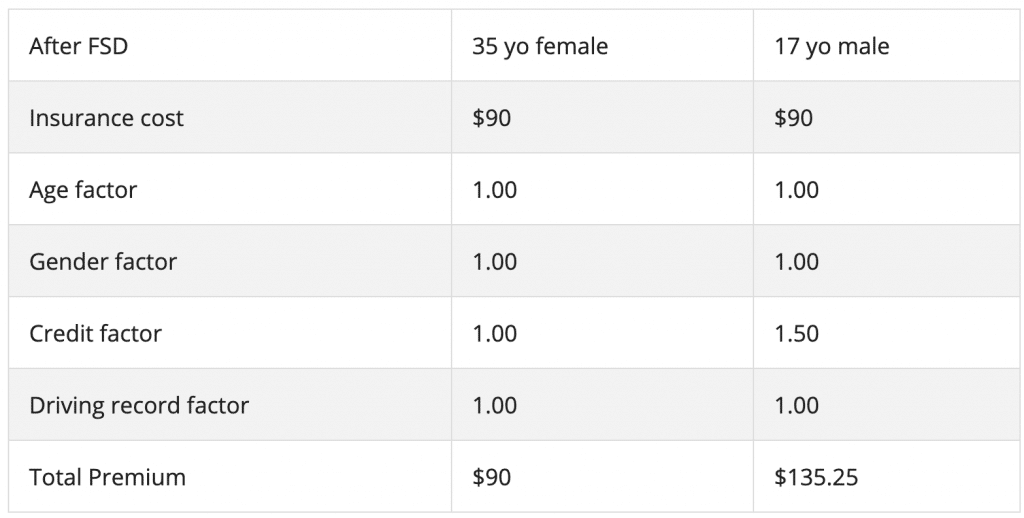

The 17 yo male class will see a reduction in premiums by 76% in our hypothetical example. Why so much? The reason is FSD will not care about your age, or your gender, or your driving record. The car does the driving, not you. These factors disappear. The insurance company will care about your credit, since they want to make sure you are good to pay your premiums every month. Anyone who pays higher premiums or is in a higher risk class will now have a strong incentive to switch to FSD.

What is the impact to the auto insurance industry?

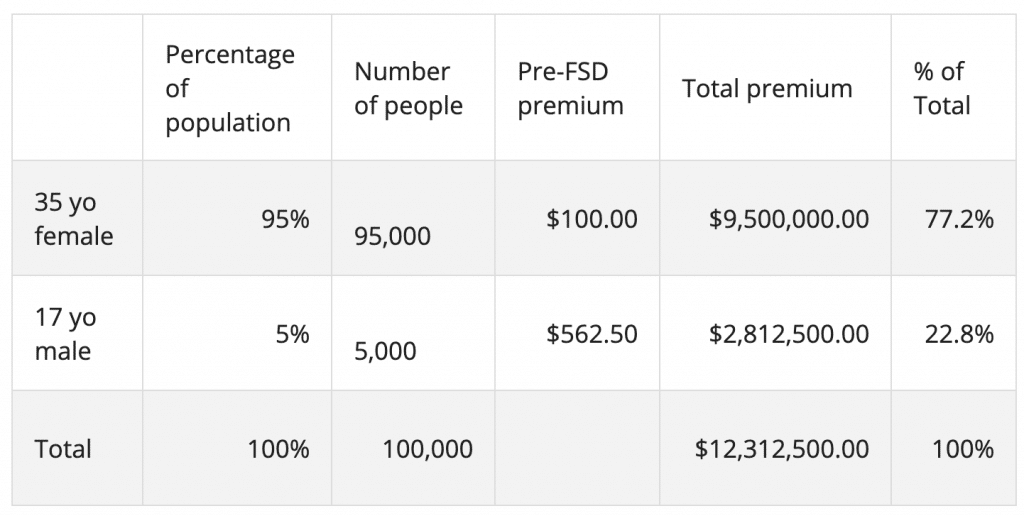

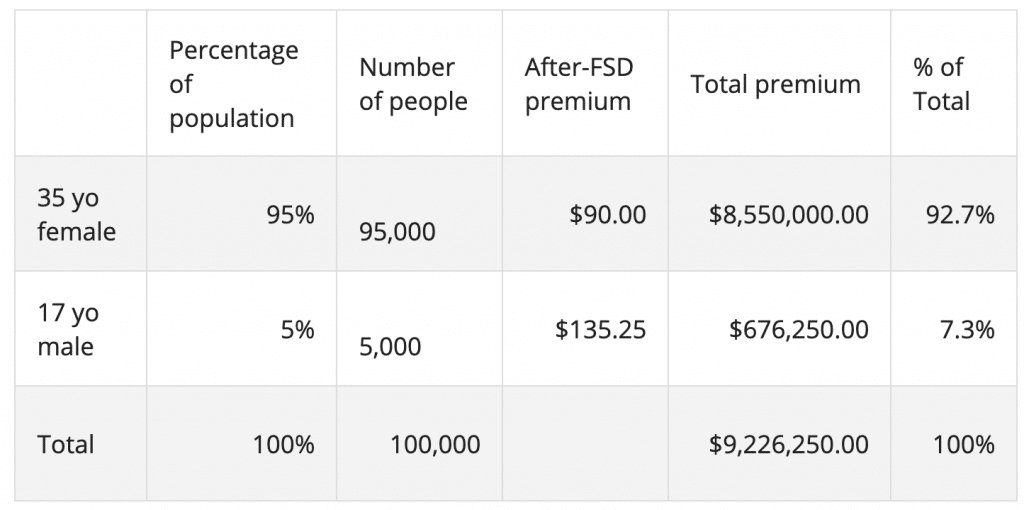

If the entire population of individuals were 35 yo females, it’s easy to see premiums will be permanently reduced by 10%. We know that is not the case in this universe. Let’s use a simple example to estimate the impact that 17 yo males are 5% of the population. Our little example will have 100,000 living in a town.

Even though the 17 yo male population is 5% of the total, because of the high premiums they pay, they account for 22.8% of pre-FSD premium. What happens after FSD?

FSD will lead to -25.1% drop in premiums in our thought example. This is most likely a permanent reduction. If the percentage of higher risk drivers is more, the drop will be more severe.

How do Telematics reduce insurance premiums?

I will make the simple assumption that an FSD will be a supercomputer on wheels. It is a supercomputer on wheels that will have many sensors and capture thousands of data points every second.

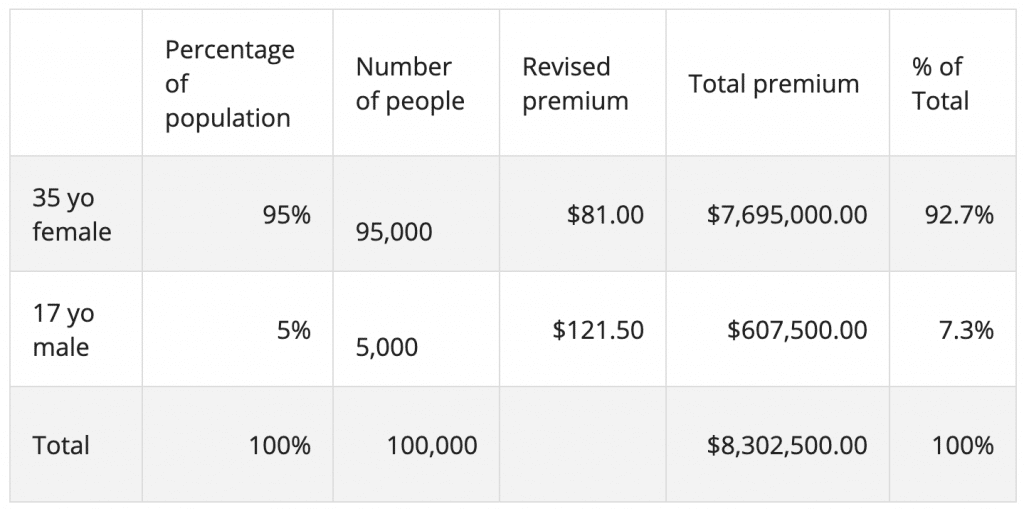

Suppose after 1 year, the company making the FSD vehicles realizes certain parts are costing more in claims than they should. They re-design their production process to make it easier to fix the problem area. This leads to a reduction in average cost of claims by 10%. In our thought example, that means the average cost of claims drops to $1800. Our base premium becomes 4.5% * 1800 = $81, 19% lower than our starting premium. What happens to our population of 100,000 drivers?

This leads to a catastrophic drop in auto insurance premiums by -32.5%. Look at my first paragraph. There are billions of dollars sent to auto and motor insurance companies every year. They employ tens of thousands of people. There is no way they are prepared to lose almost one third of their premiums every year. It doesn’t matter when it happens; when it does, the impact will cascade through their company and the larger economy. The benefit to ordinary folks of our small town are they are $4 million richer. They can save it, spend it, invest it, however they like.

This is a simple example of telematics. It will take a ream of actuaries many years to go through 10,000 different variables and figure out which ones have any predictive power and which ones can be discarded. Regulators will be a decade behind in approving the new insurance rating plans using these models and variables. These are variables that could never have been used before. How long in time is your commute? How much is spent between local and highway roads? Do you use FSD during peak traffic hours or off-peak hours? Are you using FSD to travel between different metro areas? There is the potential for redlining, which regulators will look out for. Most of what FSD and Telematics brings will be positive. Those people who are too young, too old, or with poor eyesight or health will greatly benefit from FSD.

In this piece, we haven’t discussed the reduced auto demand for vehicles once robotaxis go live. If one robotaxi can replace 3 or 4 vehicles over time, no higher power will be able to save the auto industry from losing premiums for decades to come. Driving on your own will make less and less financial sense as time goes on. Driving will become like a horse carriage driver, a quaint profession for romantic evenings. Certain well known folks have put the auto insurance industry on notice. Are they prepared?

Original Publication by Vijay Govindan at CleanTechnica.

Want to buy a Tesla Model 3, Model Y, Model S, or Model X? Feel free to use my referral code to get some free Supercharging miles with your purchase: http://ts.la/guanyu3423

You can also get a $100 discount on Tesla Solar with that code. No pressure.