Following Tesla’s (NASDAQ: TSLA) second-quarter Earnings Call that took place on Monday evening, analysts tasked with following the automaker’s stock have revised their price targets, working to unravel the massive beat that the company reported. Here is a quick rundown of what a few analysts are saying and how their outlook of the stock has changed after Tesla’s Q2 2021 Earnings Call.

CANACCORD GENUITY: JED DORSHEIMER LOWERS TESLA PT, MAINTAINS ‘BUY’ RATING

Dorsheimer lowered his price target on Tesla to $768.00 from $812.00, maintaining a “Buy” rating on the stock. Impressed with Tesla’s “surprisingly strong Q2,” Dorsheimer and fellow analysts stated that Model Y builds from Germany and Texas will equip the 4680 cells Tesla has long worked to perfect. Energy generation and storage revenue doubled from Q1, and the selling-out of Megapacks until 2023 outlines a drastic need for Tesla’s energy products. However, the main concern moving ahead for Canaccord is “increased chip shortage concerns highlighted on the Earnings Call.”

Tesla did indicate that engineers had worked to create new configurations of controllers to combat semiconductor shortages.

The company stated:

“Our team has demonstrated an unparalleled ability to react quickly and mitigate disruptions to manufacturing caused by semiconductor shortages. Our electrical and firmware engineering teams remain hard at work designing, developing, and validating 19 new variants of controllers in response to ongoing semiconductor shortages.”

Dorsheimer holds a 55% success rate and an average return of 32.9%, according to TipRanks. He is ranked 213th out of 7,609 analysts.

RBC CAPITAL: SHANGHAI’S EXPORT “HUB,” AUTO GM EX-CREDITS HIT RECORD

RBC Capital analyst Joseph Spak raised Tesla’s price target to $745 from $718 with a “sector perform” rating.

Spak said, “Volumes were higher, but cost improved. In particular, we believe a good part of this improvement is because Tesla is now using Shanghai as the ‘primary vehicle export hub.’” Additionally, Tesla’s reports of Auto GM ex-credits hit a record of 25.8%, which was +380bps q/q, +710bps y/y, according to StreetInsider (per @SawyerMerritt).

Spak has a 53% success rate with an average return of -8.3%. He is ranked 7,456 out of 7,609 analysts on TipRanks.

CFRA: INCREASE TO $675 FROM $650

CFRA analysts raised their outlook on TSLA stock by only $25 after the wildly successful earnings report, but the outlook is positive. “The beat was driven by a stronger-than-expected top line and margins, as revenue rose 90% to $11.96B ($560 above consensus) and auto gross margin expanded 300 bps to 28.4% (230 bps above consensus.).”

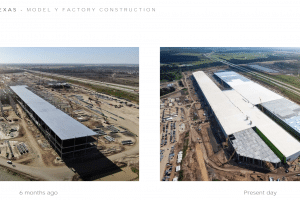

Tesla’s anticipated forecast to begin Model Y production at Berlin and Austin by EoY 2021 is also highlighted by CFRA, especially considering falsified reports that Musk’s inner circle expected Berlin to not begin production until early 2022, months later than originally expected.

CFRA maintains a “Hold” rating on Tesla stock.

At the time of writing, TSLA shares traded at $636.24, down 3.25%, despite the company’s strong Q2 earnings.