Key Takeaways

- Jim Cramer declares Tesla is a robotics company, not a car company, echoing CEO Elon Musk’s vision from the Q4 Earnings Call.

- Tesla transitioning from automotive focus to AI, robotics, Cybercab, and Optimus humanoid robots.

- Despite beating Q4 earnings numbers, stock fell 3% due to high capex and lack of new business details.

- Model S and Model X to be discontinued after Q2, as they don’t fit future autonomy plans.

- Cramer quotes: Excited about Cybercab and robots, shifts from disliking as car company to “buy, buy, buy” as robotics juggernaut.

- Tesla shares trading at $423.69, down less than 0.5%, aligning with permabull investor sentiment.

In a stunning reversal that’s got Wall Street buzzing, legendary CNBC host Jim Cramer has declared Tesla (TSLA) “actually a robotics company” – echoing what Elon Musk and Tesla’s die-hard fans have been shouting from the rooftops for years. ❶ ❷ This isn’t just hype; it’s backed by Tesla’s latest Q4 2025 earnings call, where the company laid out its bold shift away from traditional cars toward AI, autonomy, Cybercabs, and the Optimus humanoid robot. Despite beating earnings expectations, shares dipped over 3% post-earnings due to hefty capital expenditures and calls for more details on these moonshot projects. ❸ As of publishing, TSLA trades at $423.69, down less than 0.5% – a potential buying opportunity for those who see the robotics revolution unfolding. ❶

As a seasoned tech and EV investor blogger who’s tracked Tesla since its early days, this pivot feels like the caterpillar-to-butterfly moment Musk has long promised. Traditional automakers like Ford and GM are scrambling in the rearview mirror, while Tesla races toward a $10 trillion future in AI and robotics. Let’s dive deep into the details, Cramer’s flip-flop, the tech behind it, risks, and why you might want to load up now.

Tesla’s Q4 2025 Earnings: Solid Numbers, Seismic Shift

Tesla’s Q4 2025 results were a mixed bag on paper but revolutionary in narrative. The company reported earnings per share of $0.50, smashing Wall Street’s $0.45 estimate, with adjusted income holding steady amid a tough EV market. ❹ Free cash flow hit $1.4 billion, and full-year capex clocked in at $9 billion – slightly below guidance but poised to explode in 2026 as robotics ramps up. ❺

The real headline? Elon Musk confirmed the end of Model S and Model X production after Q1 or Q2 2026. These flagships, once Tesla’s halo cars, “serve relatively no purpose for the future,” Musk stated bluntly. Fremont factory lines will pivot to Optimus robot production, targeting a million units annually. ❸ ❻ ❼ This isn’t downsizing; it’s ruthless prioritization for autonomy-focused vehicles like the Cybercab.

Key Earnings Highlights:

- Beat on EPS and cash flow, but automotive margins squeezed by competition and price cuts.

- Capex surge ahead: $20B+ planned for 2026 on AI training, robotaxis, and Optimus scaling. ❽

- Narrative dominance: Musk reiterated, “We’re an AI and robotics company,” dismissing EV commoditization.

Stock reaction? A 3%+ drop the next day, as investors digested higher spending without immediate robotaxi timelines. But after-hours surges followed on robotics buzz, per Cramer. ❾

Jim Cramer’s Epic Flip: From Car Company Skeptic to “Buy, Buy, Buy” Believer

Cramer’s Mad Money rants are legendary – and often wrong-footed on Tesla. But post-earnings, he nailed the shift:

“Last night, I heard a disastrous car company speak. Turns out it’s actually a robotics and Cybercab company, and I want to buy, buy, buy. Yes, Tesla’s the paper that turned into scissors in one session. I didn’t like it as a car company. Boy, I love it as a Cybercab and humanoid robot juggernaut. Call me a buyer and give me five robots while I’m at it.” ❷ ❿

He dismissed earnings numbers: “Nobody cares about the numbers here, as electric vehicles are the past.” Musk acolytes and permabulls have preached this for years – Tesla isn’t Ford 2.0; it’s Boston Dynamics meets Uber. ⓫ Cramer even predicts the stock could go “sky high” if the robotics narrative sticks. ⓬

This aligns with bullish analysts eyeing $500+ targets if robotaxis scale, versus $350 on delays. ⓭

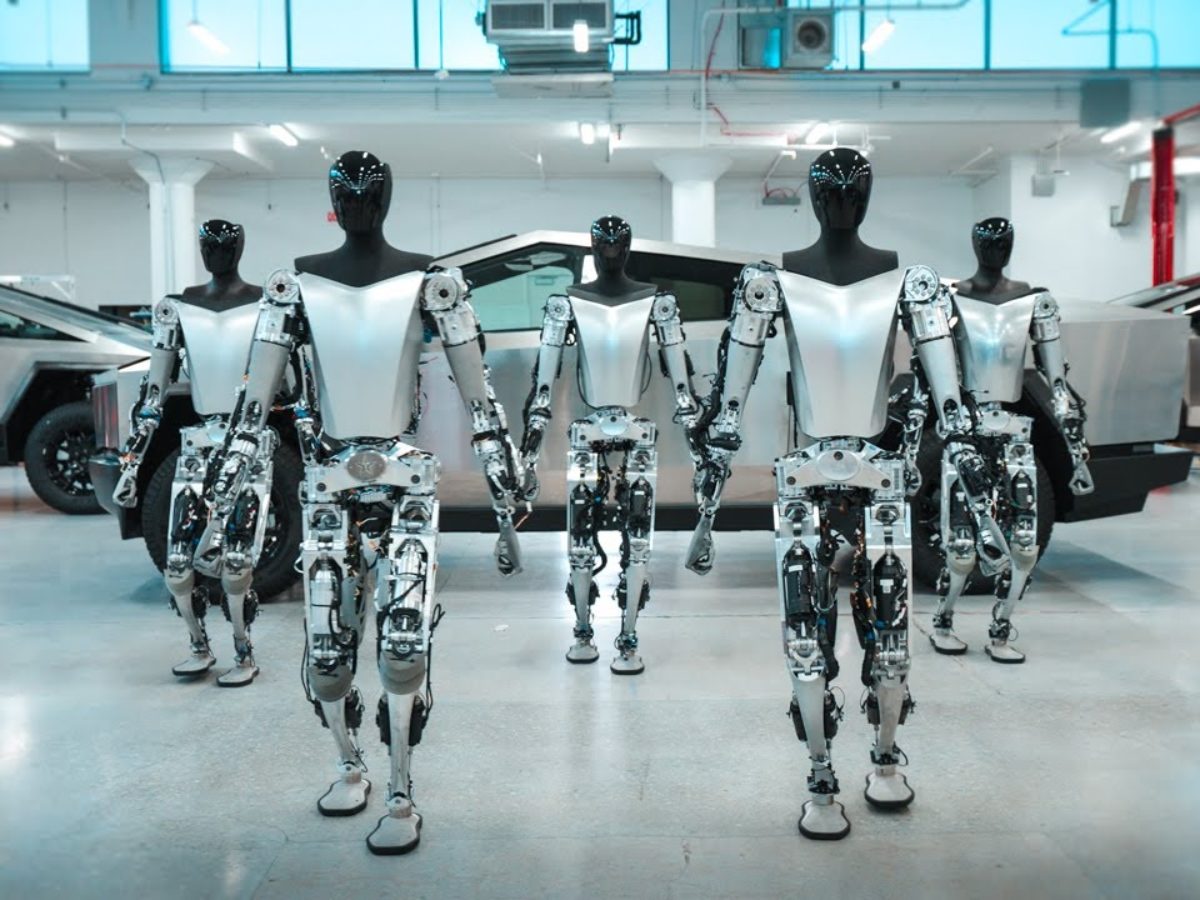

The Robotics Arsenal: Optimus and Cybercab Take Center Stage

Tesla’s not pivoting; it’s accelerating into a multi-trillion-dollar market.

Optimus: The Humanoid Game-Changer

Optimus Gen 2 wowed with folding shirts and walking demos, but 2026 is ramp-up year:

- Gen 3 reveal in Q1 2026, with sales to external customers by end-2027. ⓮ ⓯

- Gen 4 production at Giga Texas: Higher volume than Fremont’s 1M-unit line, repurposed from S/X. ⓰

- Progress accelerating: New capabilities like precise manipulation shown late 2025. ⓱

Musk eyes Optimus for factories first, then homes – unsafe, repetitive tasks. Market potential? Trillions, dwarfing EVs.

Cybercab Robotaxi: Autonomy Unleashed

The $30K two-seater sans wheel/pedals:

- Volume production 2026, with early output “agonizingly slow” then ramping. ⓲

- Testing spotted in Bay Area; Austin service since June 2025. ⓳ ⓴

- Robotaxi app live for updates; fleet revenue via subscriptions.[21]

This network could generate recurring billions, turning cars into assets.

Why the Stock Dip? Opportunity Knocks for Long-Term Bulls

High capex spooked shorts, but:

- EV slowdown temporary: China competition fades as Tesla leads in autonomy.

- Permabull alignment: Cramer’s buy call validates the thesis.[22]

- 2026 catalysts: Optimus demos, Cybercab launches, potential rate cuts boosting growth stocks. ⓭

Tesla vs. Legacy Auto: Apples to Humanoids

Ford/GM chase EVs; Tesla builds the OS. Shares belong in AI peers like NVDA, not Detroit.

Comparison Table:

| Metric | Tesla (2026 Outlook) | Ford/GM |

|---|---|---|

| Core Business | AI/Robotics | Internal Combustion/EVs |

| Growth Driver | Robotaxi/Optimus | Trucks/SUVs |

| Capex Focus | $20B+ Autonomy | $10B EVs |

| Valuation Multiple | 100x Forward | 5-7x |

Risks: Don’t Bet the Farm

- Timeline slips: Musk’s history (Cybertruck delays).[23]

- Regulation: FSD approval hurdles for robotaxis.

- Competition: Waymo, Figure AI in robotics.

- Execution: Fremont pivot success critical.[24]

Investor Advice: Play the Long Game in 2026

- Buy on dips: $400-450 entry for 2-5x upside by 2030.

- Dollar-cost average: Volatility from news flow.

- Diversify: 5-10% portfolio allocation; pair with NVDA, ARM.

- Watch milestones: Q1 Optimus reveal, Cybercab volume.

- Ignore noise: Cramer’s buy signal > short-term wiggles.

Tesla’s robotics bet could mint millionaires – or bust if delayed. But with Musk at helm and Cramer converting, momentum builds.

What do you think? Bullish or wait-and-see? Drop comments below!